What founders and investors need to know about the US livestream commerce opportunity

The 3 waves of US livestream commerce, the 3 Business Drivers, the 3 Stakeholders' Jobs to be Done & where QVC is now.

Contents

High-Level drivers of Livestream Commerce

Understanding the historical context: The US Livestream Commerce Landscape

Business Driver #1: Building Trust by matching Product to Platform

Business Driver #2: Building a Call-to-Action

Business Driver #3: Sales through Entertainment

The 3 Stakeholders’ Jobs to be Done Framework

The bull case for livestream commerce: Comparison to QVC

If you are reading about live streaming commerce — you probably know the headline basics. It is huge in China at 600B USD GMV. In 2020 GMV Douyin did 60B, Kuaishou did 51B, Taobao Live did 62B. It is emerging in the US. You are trying to find a more comprehensive breakdown on where this industry will go next.

In this article, we wanted to lay out the historical context of livestream commerce, the competitive landscape today, a framework for understanding the business model, specifically its main levers for success and what the end-state business model looks like (diving into the economics of QVC)

If you are a child of the ’80s or ’90s, you probably remember QVC or the Home Shopping Network. Before every retailer had a website, and before Amazon became the “everything store,” people who wanted to shop without leaving the house would turn to one of those cable channels for programming designed to sell products to them.

High-Level drivers of Livestream Commerce

Livestream commerce has its origins in the distinct but related concepts of trust and entertainment. Livestream commerce finds its niche in low-trust products - agriculture and cosmetics. You could fall sick by eating fruits with too much pesticides, or have fruits with bad taste/sugar levels. You could also ruin your skin with sub-quality cosmetics.

The best framework to think about it is as an agency business model with a payments interface. The three main drivers in this business is its ability to attract, with the right incentives, influencers who know how to sell and entertain via livestreaming, and as a platform, strike the best deals with the most exciting brands/SKUs, and a user interface that will encourage seamless conversions.

A16Z describes ‘shopatainment’ as part art, part game show, part theater, part supply chain management, and part auction house , which is not far from it - though as we will see, a familiar agency-type business dynamic will emerge.

Livestream commerce sees significantly better performance than traditional e-commerce, and this can be seen in the customer behavior numbers. Conversion rates are higher:

As noted by 6Pages, conversion rates can be 30-40% – dramatically higher (up to 10x) than traditional ecommerce. One livestream-shopping marketplace reported that nearly 80% of customers made a 2nd purchase within 30 days. Companies are also reporting a 50% lower product return rate because consumers can ask questions and see sizes and colors.

Understanding the historical context: The US Livestream Commerce Landscape

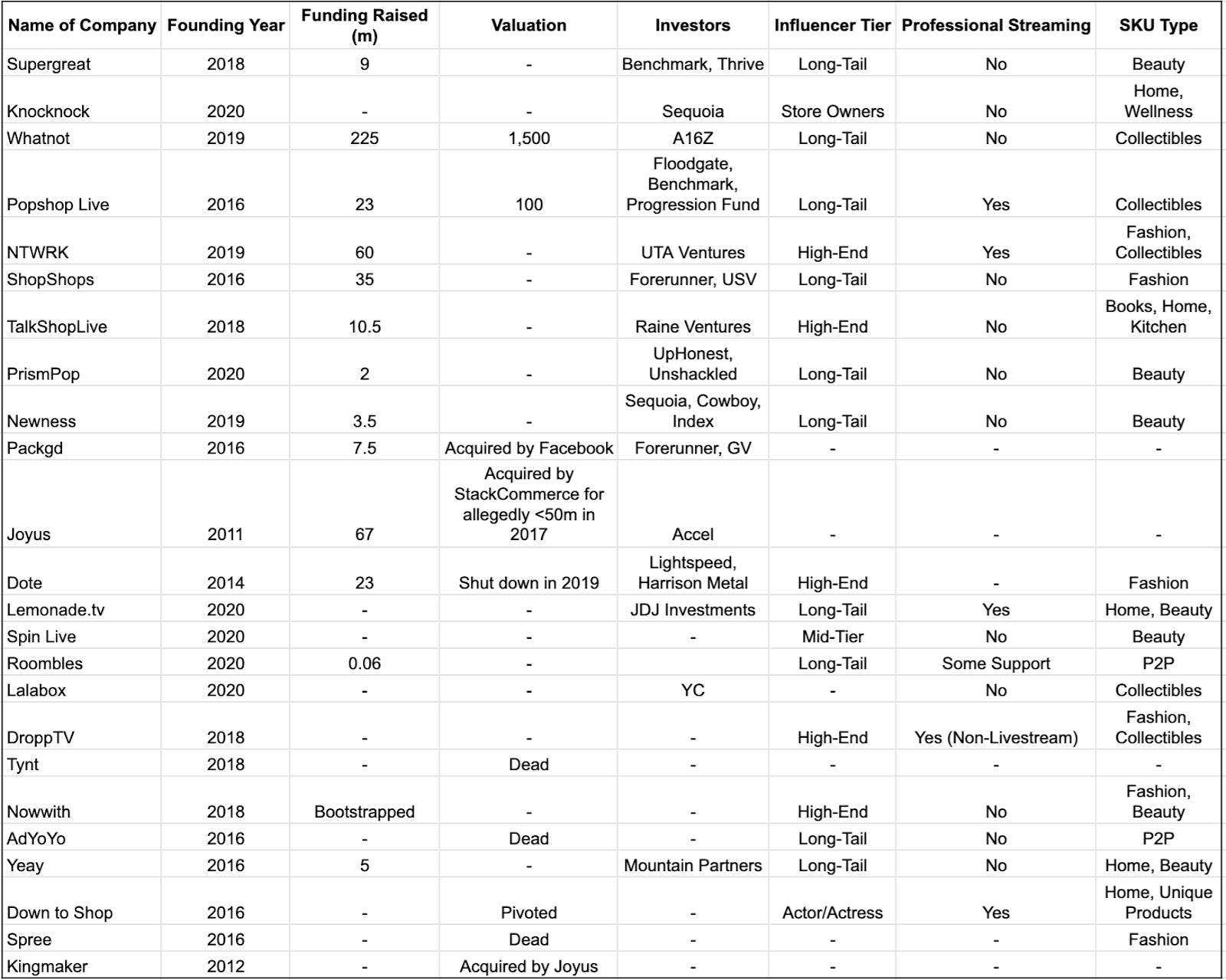

We can break down the different types of US livestream commerce business models by their focus on Influencer Tiers, Use of Professional Streaming, and SKU focus.

In the competitor’s scan for US livestream commerce plays, we note three major waves of players:

Wave 1: The first wave of legacy television commerce players: QVC, Home Shopping Network

Wave 2: The 2010-16 Post-FB social network boom of players: Joyus, Dote, Down to Shop

XiaoHongShu becomes a unicorn in 2016

Wave 3: The 2018 re-emergence: NTWRK, TalkShopLive

Snapchat IPOs, Facebook Stories launched in 2017

Chinese business models become an area of attention for US markets as Pinduoduo IPOs in 2018.

Bytedance acquires Musical.ly in 2017 and explodes in popularity in the US

There are 3 main takeaways to think about when we looked at the US competitive landscape.

Firstly, breakout winners have come from collectibles, and we will see more winners emerge in Beauty - cosmetics and skincare specifically.

Secondly, there is a diversity of players within the influencer tier and I was particularly intrigued by the use of store owners livestreams. Though bullish on their selling capability, I was less-bull on their entertainment quality. Here, flash sales and gamification tactics are likely to feature more heavily as a hook.

Lastly, livestream commerce is not new even in the US, and I remain fully bullish on standalone livestream commerce plays to develop and win in niches, expand horizontally and win big.

Matthew Lee, Partner at Progression Fund, notes that Wave 1 of QVC & HSN were largely successful as they pioneered the TV/cable medium for 35-64 year old women, many of whom were stay at home mums with an average age of 50. Wave 2 was likely unsuccessful because mobile penetration was not super high yet, and live content was extremely hard. The content needs to engage users immediately otherwise they would leave, so the market timing was not right and the tech stack was likely emerging.

From a timing perspective, Wave 3 is focused on a younger, mobile-first audience who want engaging and interactive experiences. Matthew notes that a lot of the companies in the above list did not start with livestreaming, but were early movers in adopting it, accelerated by the pandemic and the significantly higher conversion rates that livestream commerce offered.

Business Driver #1: Building Trust in the SKU

While there are more consumers shopping via e-commerce than ever before, most users still feel unsure about buying products from websites they haven’t shopped on or heard of before. A major reason for that is the fact that people are used to being able to see the product in person before buying it, or at least have someone they can talk to and ask questions. On most e-commerce websites, you’d be lucky to get a bot to answer your questions.

Livestream commerce is about real-time interaction as a vehicle to build trust. This makes livestream commerce a perfect vehicle to attack lower-trust SKU commerce. You are no longer buying a product off a static page. You are able to see someone speak about the product, and explain to you why it is right for you personally after building an element of a trusting relationship. Taking it one step further than just watching them speak about it like on the yesteryear TV shopping networks, you are even able to interact with them and ask them questions about the product. In a world where human contact is becoming increasingly rare while shopping, livestream commerce is able to bring a human element that significantly boosts trust and enables stronger brand loyalty.

“People want to buy something from someone they trust. I have established that trust with the viewer,” Martin told Fast Company, which may sound vague and unprovable, except that NBC’s in-house analytics show that sales on its e-commerce platform go up whenever a product is associated with an image of her face.” - Vox

If we dive into the concepts of trust, we see that trust correlate strongly with certain SKUs more than others.

This is also reflected in the SKU categories, which generally require an education process to overcome a trust deficit:

The top category for Kuaishou is jewellery - specifically gold bars and emeralds, which is a historically opaque industry. The top 3 categories for Douyin are clothing, personal care and make-up. Xiaohongshu has also been able to specifically target foreign brands looking to enter China and overcome a trust deficit.

As an aside, Fashion, specifically women’s clothing, are likely to pop up as a common SKU for influencers. However, I would argue for example that early-stage livestream commerce companies will face significant supply-chain challenges tackling fashion due to the increased complexity of maintaining a fashion supply chain and interface. Fashion is far more likely to succeed if promoting a limited line of SKUs with small size variations (i.e. shoes).

Nicole Quinn, General Partner at Lightspeed Venture Partners, holds a view on the type of SKUs that are most likely to succeed in video commerce:

The key for all forms of live shopping is to lean into collectibles. The powerful part of collectibles is that it taps into human behavior where you cannot get enough of them. With a high willingness to pay, there is a strong competitive element that produces strong emotions just as pride, envy or jealousy. Collectibles are a large part of how QVC / HSN began and it is now a key driver for the online live shopping companies we see emerging today.

Trust and Entertainment, go hand in hand with community building. This is particularly apparent in SKU categories like collectibles, and cosmetics, where we see parallels in Whatnot/Popshop.Live (Collectibles) to Bilibili and Supergreat (Beauty) to Xiaohongshu.

It can be noted that livestream commerce can also be introduced to a wide array of non-traditional e-commerce SKUs, for example of cars, houses, etc, in ways that would not have been possible on a QVC-type physically closed-set. In a similar vein, we have already seen the rise of Tiktok Financial Influencers who talk about various publicly traded stocks through livestreams, with online brokerages like FUTU embedding livestream capabilities for their influencers within their forums (which recently got banned a few days ago).

Business Driver #2: Building a Call-to-Action

“But if you call now, within the next twenty minutes cause we can't do this all day, we'll give you a second set absolutely free.”

Looking past the haunting eyes of Vince Offer (pictured above), the infamous ShamWow infomercial pitchman, we see that one of the keys to conversion of video commerce to purchase is a time-based call to action.

Given the nature of livestream commerce, it is easy to scroll past into the next video, or be satisfied at the entertaining nature of the pitch itself. One of the most overlooked lessons from livestream commerce plays has been the role of time-based discounts in moving the consumer from the discovery and entertainment phase, to actual conversion.

Time-based discounts are coupons or discounts that expire in the next few minutes/hours. These discounts can be given freely or can be acquired easily through low-efforts tasks (linked to engagement for example as seen below). In substance, they are more sophisticated forms of the type of time-based FOMO that the ShamWow commercial tries to instill in their viewers.

These time-based methods can also be seen in other features like showcasing a countdown for limited quantity SKUs, higher discounts for earlier purchasors, and many others. These time-based conversion tricks are especially key for livestream commerce, given the temporal nature of the livestream where the consumer attention span is more focused, but may flip to another channel/video quickly.

Business Driver #3: Sales through Entertainment

The two core jobs to be done here are selling and entertainment.

Lindsey Li, Investor at Bessemer Venture Partners, notes that this is not new. In the US, offline commerce is often inherently social – malls are destinations to meet friends and browse or discover goods. Shopping is naturally inclined towards solving for entertainment.

The interactability function of social media has meant that, unlike a celebrity endorsement, which typically meant posing for photo shoots, filming TV advertising and doing press releases, the influencer themselves are expected to use social media, and in the case of livestreaming, to interact themselves with their fanbase in real time. This has helped shaped fan engagement in the livestreaming space into a blend of talking and selling a product, while being entertaining.

This graphic from A16Z helps explain the model of “shopatainment.”

In certain cases, brands and platforms take it one notch above. In Asia, it has focused fully as a form of entertainment. At first glance, the set and production value of a livestream is indistinguishable from a professional set. In Asia, the powerful force of video entertainment shopping has spawned a livestream ecommerce industry akin to professional movie production.

This represents an important bottleneck for platforms serving long-tail influencers. Although a seemingly attractive audience segment since it is relatively easy to acquire (e.g. mass DM’s via Instagram), the skill-sets for selling and entertainment via livstreaming is very different from posting curated images/posts via Instagram.

Long-tail influencers are far more likely to work in niches where there is a shared and baseline understanding of the products in question (i.e. collectibles, ethnic fashion) where niche influencers with non-significant audiences may have extremely sticky audiences due to the specific niche they play in.

In more competitive product segments (i.e. women cosmetics), reliance on mid-higher tier influencers may be necessary, especially in the beginning, as a means for the livestream platform to differentiate itself from others.

As an aside, long-tail influencers is where horizontal content platforms like Tiktok and Youtube have an advantage since they have a lot of data on existing influencers and their potential to scale as well as an ability to leverage cross-selling as a means to attract influencers to convert into live-stream commerce. I remain bullish on verticalized livestream commerce plays, as a function of being able to carve niches both from a viewer, brand and influencer acquisition perspective, as well as supply-chain/SKU optimisation perspective.

Matthew Lee, Partner at Progression Fund, postulates that retailers will have to deliver an omnichannel experience that includes livestream shopping because of the large increase in conversion rates compared to other existing channels. Many retailers may also find themselves turning into a media company in the coming years. In a relatively prescient move, Pinterest announced their move into livestream commerce a few days ago.

QVC has understood this and has optimized for high-end influencers on their livestream platforms. QVC hosts are personalities, many of whom have devoted fan bases, like the late comedian Joan Rivers whose QVC jewelry line sold $1 billion over 20 years.

They are trained in the products they sell, often visiting manufacturing plants to school themselves. When on air, the host juggles promoting a product and interacting with models, guest hosts, callers, and off-screen analysts. The host physically interacts with the product, highlights its features in abundant detail, and makes their sales pitch. - Moz

Between his two weekly live shows on QVC and his broad digital platform, Mr. Venable last year sold more than $250 million worth of egg poachers, frozen crab cakes and backyard smokers. When he posted a recipe for Philadelphia cheesesteak dip, it reached 5.5 million people on Facebook. The two cookbooks in his “In the Kitchen With David” series have sold more than a half-million copies on QVC. - New York Times

This blend can be complicated to pull off as can be seen in Amazon’s own failures with livestream commerce: Style Code Live.

In 2016, Amazon invested significantly in Style Code Live (SCL), a livestream commerce platform and brought on high-end influencers to sell. Lyndsey Rodrigues, Rachel Smith and Frankie Grande (Ariana’s brother) — all had TV and broadcast backgrounds before joining Amazon. Yet, it was shut down by 2017.

In a post-mortem published by Forbes, Paula Rosenblum noted that a poor understanding of the interaction between selling and entertainment brought down SCL.

Although Style Code Live was helmed by proven talent, the channel itself seemed to be a cross between a typical home shopping channel and a light daytime talk show that talked about style, fashion, and beauty tips. While Amazon did not release the number of viewers who tuned into the channel or how many sales were generated by the products sold, it does appear that the main reason for its failure was the lack of focus in combining two different TV genres.

In essence, people who enjoy shopping channels like QVC and HSN obviously got bored watching the tips and reality show aspects of the channel. Meanwhile, those who liked listening to tips and guest appearances by the likes of Kourtney Kardashian and Sarah Jessica Parker were probably turned off by the push to sell the products. Hard sell and soft sell rarely work well together, and this may have been the overriding reason why Style Code Live met its demise.

Success in the home shopping world is a result of the interaction between the host, a guest (ideally a celebrity of some sort) and the audience. Of course, the products have to matter, but the key is really that interaction. The audience has a chance to talk to the celebrity

The blend of real-time data on top of influencers enables this real-time juggling of SKUs, Brands, Influencers and Platforms.

Shawn Xu, Investor at Floodgate, notes that he "get[s] excited by the data driven selling that's possible on livestream commerce. With QVC, they are able to measure and benchmark how specific products are selling by the minute. With platforms like our portfolio company Popshop Live, we're able to get this data on an even more granular level. We are also excited by the community engagement that gets built up around individual livestream seller brands, which are driving shoppers back to the platform in a stickier way. We are super bullish about this category."

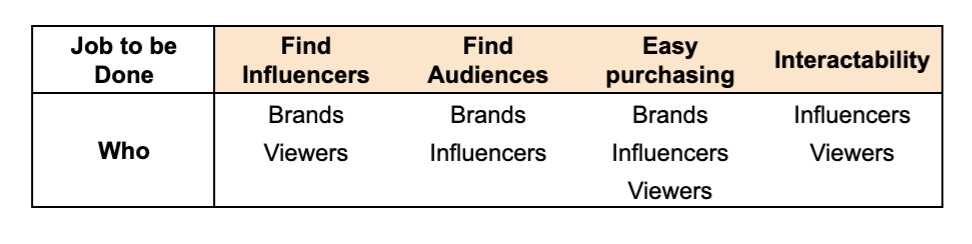

The 3 Stakeholders’ Jobs to be Done Framework

For Influencers

Provide a platform that allows me to interact with my audience, and let them seamlessly purchase, so I have higher commissions

Provide an attractive platform for Brands (and ideally introduce me to them), so they receive all the necessary data they need to be attracted to me as an influencer for them

Provide a platform that will continue to grow significant eyeballs so I can grow my fanbase when I use your platform

For Brands

Provide a platform that is easy for me to find and interact with these influencers

Provide a platform that will continue to grow significant eyeballs

Provide a platform that is easy for me to sell and ship products

Provide a platform that can help me build and engage a community

For Viewers

Provide the most relevant influencers for my tastes as fast as possible

Provide an interactive and entertaining in-show user experience

Provide a seamless purchasing experience

The key bottleneck here is the matching between influencers and brands. Interaction protocols, especially if a platform adopts long-tail influencers, and brands are still fairly nascent and platforms would need to hand-hold both influencers and brands as to why their platform is the best way to engage their audience.

As the platform’s topline is driven by successful matches between influencers and brands, a heavy amount of handholding and matchmaking between influencers and brands are likely to take place - which is heavily reflective of the agency-type dynamics that the platform would have to deal with.

From Clubhouse, we can see that taking a light engagement model, in the face of participants who may be new to this mode of engagement, is likely to be detrimental to the platform.

“Six creators from Clubhouse’s creator program say no brands sponsored them before the end of the program, and Clubhouse failed to turn any of their shows into sustainable endeavors, as it advertised it would. None of them plan to keep doing their high-production shows, and many are refocusing their efforts on other platforms, simply because they have a better shot at being compensated for their effort...

[Influencers] received the number of unique listeners, the total number of minutes spent listening, and the number of listeners a room had at its maximum. “Obviously, if you know anything about sponsorships, that means nothing to anybody,” she says.” - The Verge

The ability for platforms to provide some element of product structuring as a key component for influencer monetization has been an important point I have made before, so I will just add that A16Z has made a good list of the types of products influencers can offer on livestream platforms.

The bull case for livestream commerce: Comparison to QVC

Incumbents are massive and are not slowing down. QVC, the largest US incumbent, generated $11.47 billion in 2020 and as early as 2015, nearly half of those sales were taking place online — The company has 16.5 million consolidated customers worldwide with strong retention. 90% of QVC’s revenue comes from loyal repeat shoppers. The average QVC shopper makes between 22-25 purchases per year.

QVC has adapted fairly well to the new consumer age, despite being a 35-year-old company. Although their focus on professional filming (similar to NTWRK) allows them to target a more mainstream audience (and if I were to guess, promotes higher AOVs), their transition into mobile commerce has been successful. In 2017, online sales made up 59% of QVC revenue in the US, and in 2018 it bounced up to 62%. Of those sales, 66% were made in a mobile app. This has placed QVC in the top 10 for e-commerce sales, including mobile sales.

Diving into QVC’s annual report, we find a fairly strong and diversified business. QVC has 16.5m customers, of which 11.6m are from the US. 26% of their revenue is international, with a Net Income of 7.4% (2020), 7.0% (2019), 7.9% (2018). Their SKU categorization is also diversified across a large number of categories, with Home (42% of sales) and Beauty (18% of sales) coming on top.

The legacy nature of their business can be evident in a few areas. Besides a high executive compensation (2020: ~17m to the Exec Chairman and ~10m to the CEO) for a 4B market cap company with no significant long-term shareholder value capture, the year on year revenue growth has essentially been flat, growing 2% in 2 years (and during COVID on top of that).

In my view, it is notable that QVC, like their Chinese counterparts, is owning live stream mindshare for more mainstream SKUs like Home and Beauty. As US livestream commerce startups mature from collectibles and fast-fashion into more mainstream SKUs, we will see QVC’s lunch being eaten by many VC-backed startups leveraging the livestream commerce opportunity.

Looking at the financials and operational numbers of QVC made me extremely bullish that there are at least several multi-billion dollar profitable GMV companies that could be created in the short run within the livestreaming space alone. We are in the early days of this latest wave of US livestreaming, and I am super excited about what is to come.

Thanks to Professor Rajiv, Lindsey Li, Matthew Lee, Nicole Quinn, Akshay Bajaj, Shawn Xu, Shawn Teow for comments/input! Input does not constitute endorsement.

Really fascinating piece